Resources

About Us

Low-Carbon Cement Alternatives Market Size, Share & Growth Analysis | By Product Type, Raw Material, Application & End User | Global Forecast 2025-2032

Report ID: MRCHM - 1041479 Pages: 225 Apr-2025 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportReport Overview

This comprehensive market research report analyzes the rapidly expanding low-carbon cement alternatives market, evaluating how emerging sustainable materials are addressing carbon emission challenges across the construction industry. The report provides a strategic analysis of market dynamics, market size and forecast till 2032, and competitive positioning across global and regional/country-level markets.

Key Market Drivers & Trends

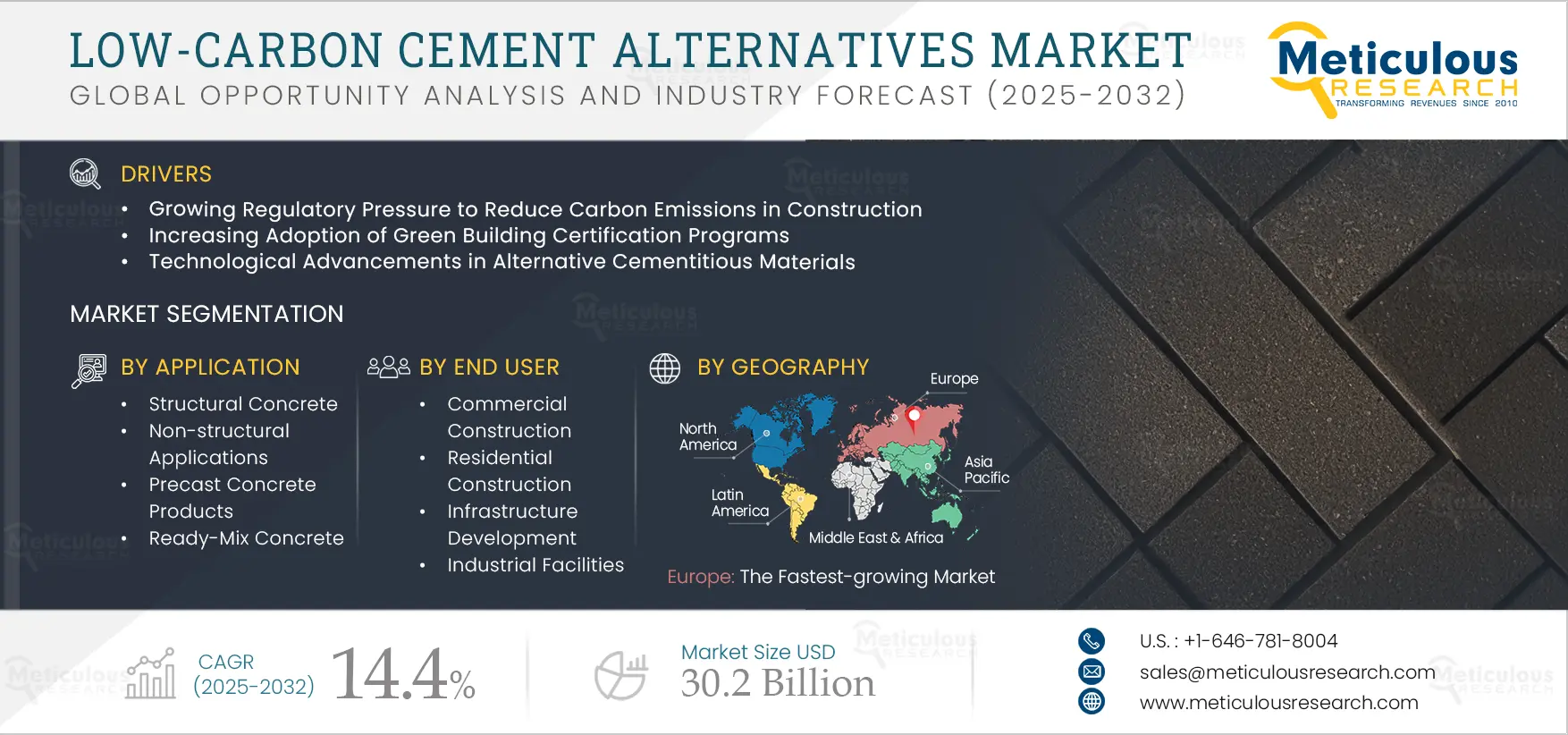

The low-carbon cement alternatives market is primarily driven by growing regulatory pressure to reduce carbon emissions in construction, increasing adoption of green building certification programs, rising corporate sustainability commitments in the construction sector, technological advancements in alternative cementitious materials, and growing awareness of embodied carbon in building materials. The shift toward blended cements with reduced clinker content is reshaping the industry, while increasing research in alkali-activated materials and geopolymers is gaining significant traction. Additionally, integration of digital technologies for optimized mix designs, emergence of carbon curing technologies, and rise of bio-based additives and alternative activators are further driving market growth, especially in Europe and North America.

Click here to: Get Free Sample Pages of this Report

Key Challenges

The overall low-carbon cement alternatives market faces some challenges including higher production costs compared to traditional Portland cement, limited availability of alternative raw materials in some regions, slower setting and strength development of some alternatives, conservative industry standards and building codes, and limited large-scale production capacity for novel alternatives. Additionally, ensuring long-term durability and performance, overcoming industry resistance to new materials, scaling production while maintaining carbon reduction benefits, standardization and certification of novel cement types, and educating stakeholders on proper use and specifications present significant barriers, potentially slowing down market penetration in different countries across the globe.

Growth Opportunities

The low-carbon cement alternatives market offers several high-growth opportunities. Carbon pricing and taxation mechanisms favoring low-carbon materials are creating economic incentives for wider adoption. Another major opportunity lies in public infrastructure projects specifying low-carbon concrete. Additionally, valorization of industrial by-products in cement production is creating circular economy benefits while reducing costs. The development of carbon capture and utilization technologies and growing market for carbon-negative construction materials further expand the growth landscape for both established manufacturers and innovative startups.

Market Segmentation Highlights

By Product Type

The Supplementary Cementitious Materials (SCM) Blends segment is expected to dominate the overall low-carbon cement alternatives market in 2025, primarily due to their established performance record, relative ease of implementation within existing production systems, and familiarity among construction professionals. These materials offer a practical balance between carbon reduction and technical performance, with widespread regulatory acceptance. The Geopolymer Cement segment follows closely, particularly in regions with abundant industrial by-products suitable for alkali activation. However, the Calcium Sulfoaluminate Cement (CSA) segment is expected to grow at the fastest CAGR through 2032, driven by its superior early strength development, reduced energy requirements during manufacturing, and increasing commercial availability.

By Raw Material

The Industrial By-products segment (including fly ash, slag, and silica fume) is expected to hold the largest share of the overall low-carbon cement alternatives market in 2025, due to their widespread availability as waste streams from power generation and metal production, established supply chains, and proven performance as supplementary cementitious materials. The Calcined Clays segment follows closely, driven by abundant natural reserves and growing interest in limestone calcined clay cement (LC3) technology. However, the Alternative Calcium Sources segment is expected to grow at the fastest rate during the forecast period, propelled by innovations in carbon-negative materials that sequester CO2 during production and the development of novel binding agents derived from waste streams.

By Application

The Ready-Mix Concrete segment is expected to hold the largest share of the overall low-carbon cement alternatives market in 2025, primarily due to its widespread use in construction projects of all sizes, the ability to precisely control mixture proportions in centralized facilities, and the sector's strong emphasis on sustainability certifications. The Precast Concrete Products segment follows closely, benefiting from controlled manufacturing environments that can accommodate variations in setting times and curing requirements. However, the Structural Concrete segment is expected to experience the fastest growth rate during the forecast period, driven by increasing performance validation of alternative cements for load-bearing applications and the high visibility of green building projects employing sustainable structural materials.

By End User

The Commercial Construction segment is expected to hold the largest share of the overall low-carbon cement alternatives market in 2025, primarily due to corporate sustainability initiatives, green building certification requirements, and the high visibility of sustainable corporate headquarters and facilities. The Infrastructure Development segment follows closely, bolstered by government procurement policies increasingly specifying low-carbon materials for public works. However, the Industrial Facilities segment is expected to grow at the fastest rate during the forecast period, driven by heavy industries seeking to reduce scope 3 emissions in their physical assets, requirements for specialized performance characteristics, and the symbolism of using sustainable materials in manufacturing settings.

By Geography

Europe is expected to hold the largest share of the global low-carbon cement alternatives market in 2025, driven by stringent carbon regulations, well-established carbon pricing mechanisms, and ambitious climate targets across the region. Additionally, strong green building certification programs and consumer awareness contribute significantly to market dominance. North America follows as the second-largest market, bolstered by corporate sustainability initiatives and growing state-level procurement policies requiring low-carbon materials. However, the Asia-Pacific region is witnessing the fastest growth rate during the forecast period, primarily driven by rapid urbanization, massive infrastructure development, and increasingly stringent environmental regulations in countries like China and India.

Competitive Landscape

The global low-carbon cement alternatives market features a diverse competitive landscape with established cement manufacturers pivoting toward sustainable solutions, specialized green material startups, technology providers focused on carbon capture and utilization, and research institutions commercializing novel binding technologies.

The broader manufacturing landscape is categorized into industry leaders, market differentiators, vanguards, and contemporary stalwarts, with each group employing distinctive strategies to advance sustainable construction materials. Leading manufacturers are balancing incremental improvements to existing cement formulations with investments in breakthrough technologies that promise deeper decarbonization.

The key players operating in the global low-carbon cement alternatives market are Holcim Group, HeidelbergCement AG, CEMEX S.A.B. de C.V., CRH plc, Solidia Technologies, Carbicrete, CarbonCure Technologies Inc., Ecocem Materials Ltd., Calix Limited, Ceratech Inc., BioMason Inc., Terra CO2 Technologies, CarbiCrete, Zeobond Pty Ltd, and LC3 Technology among others

|

Particulars |

Details |

|

Number of Pages |

225 |

|

Format |

PDF & Excel |

|

Forecast Period |

2025–2032 |

|

Base Year |

2024 |

|

CAGR (Value) |

14.4% |

|

Market Size (Value) in 2025 |

USD 10.3 billion |

|

Market Size (Value) in 2032 |

USD 30.2 Billion |

|

Segments Covered |

|

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, France, U.K., Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Rest of Latin America), Middle East & Africa (Saudi Arabia, United Arab Emirates, Rest of Middle East & Africa) |

|

Key Companies |

Holcim Group, HeidelbergCement AG, CEMEX S.A.B. de C.V., CRH plc, Solidia Technologies, Carbicrete, CarbonCure Technologies Inc., Ecocem Materials Ltd., Calix Limited, Ceratech Inc., BioMason Inc., Terra CO2 Technologies, CarbiCrete, Zeobond Pty Ltd, and LC3 Technology |

The global low-carbon cement alternatives market was valued at $8.4 billion in 2024. This market is expected to reach $30.2 billion by 2032 from an estimated $10.3 billion in 2025, at a CAGR of 14.4% during the forecast period of 2025–2032.

The global low-carbon cement alternatives market is expected to grow at a CAGR of 14.4% during the forecast period of 2025–2032.

The global low-carbon cement alternatives market is expected to reach $30.2 billion by 2032 from an estimated $10.3 billion in 2025, at a CAGR of 14.4% during the forecast period of 2025–2032.

The key companies operating in this market include Holcim Group, HeidelbergCement AG, CEMEX S.A.B. de C.V., CRH plc, Solidia Technologies, Carbicrete, CarbonCure Technologies Inc., Ecocem Materials Ltd., Calix Limited, Ceratech Inc., BioMason Inc., Terra CO2 Technologies, CarbiCrete, Zeobond Pty Ltd, and LC3 Technology.

Major trends shaping the market include shift toward blended cements with reduced clinker content, increasing research in alkali-activated materials and geopolymers, integration of digital technologies for optimized mix designs, emergence of carbon curing technologies, and rise of bio-based additives and alternative activators.

• In 2025, the Supplementary Cementitious Materials (SCM) Blends segment is expected to dominate the overall low-carbon cement alternatives market by product type

• Based on raw material, the Industrial by-products segment is expected to hold the largest share of the overall low-carbon cement alternatives market in 2025

• Based on application, the Ready-Mix Concrete segment is expected to hold the largest share of the global low-carbon cement alternatives market in 2025

• Based on end user, the Commercial Construction segment is expected to hold the largest share of the market in 2025

Europe is expected to hold the largest share of the global low-carbon cement alternatives market in 2025, driven by stringent carbon regulations, well-established carbon pricing mechanisms, and ambitious climate targets across the region.

The growth of this market is driven by growing regulatory pressure to reduce carbon emissions in construction, increasing adoption of green building certification programs, rising corporate sustainability commitments in the construction sector, technological advancements in alternative cementitious materials, and growing awareness of embodied carbon in building materials.

Published Date: Sep-2024

Published Date: May-2024

Published Date: May-2024

Published Date: Aug-2024

Published Date: Mar-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates