Resources

About Us

Gaming Accessories Market Size, Share, Forecast, & Trends Analysis by Product (Gaming Chairs, Controllers, Headsets, Keyboards), Device (Smartphones, Consoles), Technology (Wired, Wireless), Distribution Channel—Global Forecast to 2032

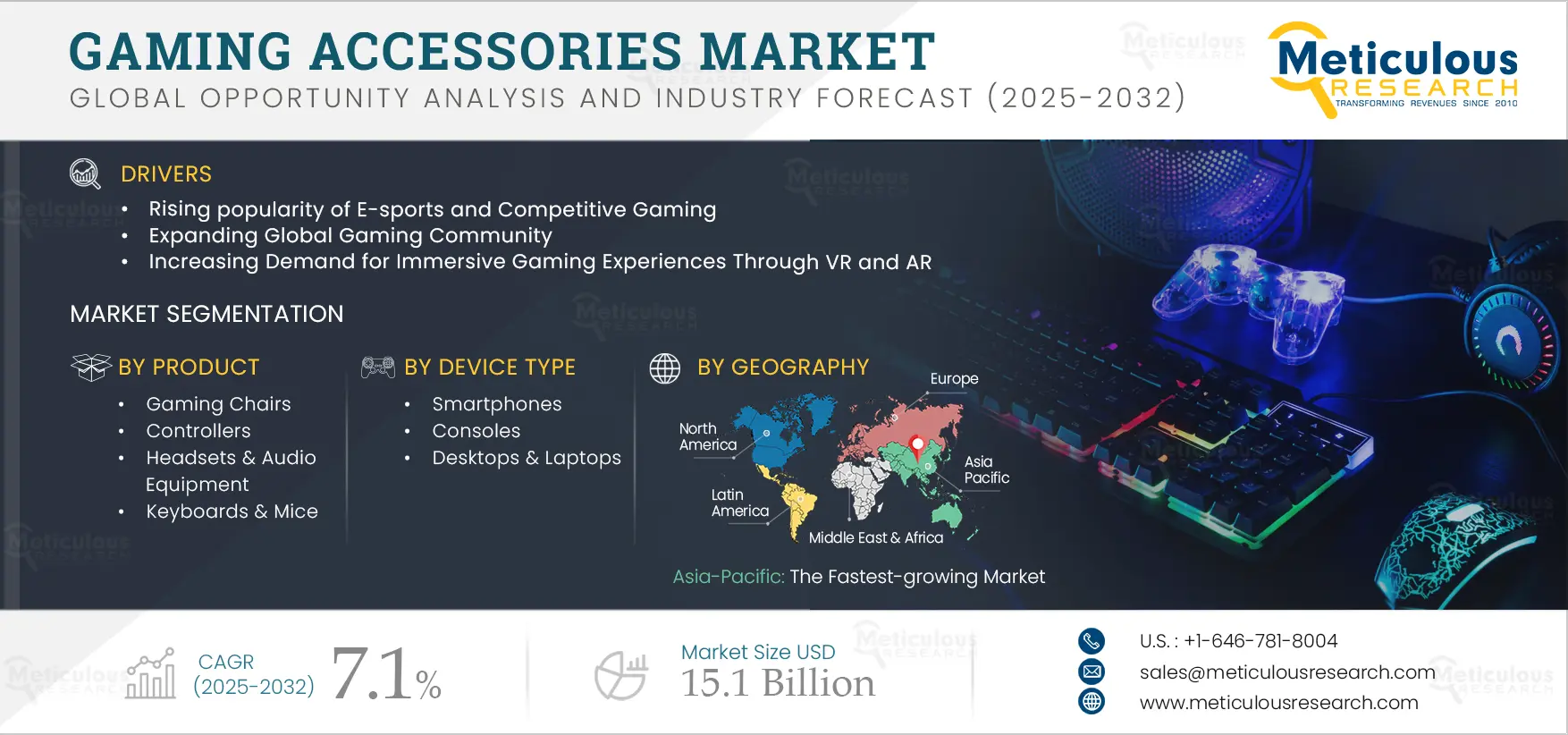

Report ID: MRSE - 1041435 Pages: 210 Dec-2024 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportKey factors driving the growth of this market include the rising popularity of e-sports & competitive gaming, the expanding global gaming community, and the increasing demand for immersive gaming experiences through VR and AR. Additionally, the rising demand for customized/personalized gaming accessories and partnerships between gaming accessory manufacturers and game developers to create branded or game-specific accessories are expected to offer further opportunities for market growth.

Click here to: Get a Free Sample Copy of this report

Click here to: Get a Free Sample Copy of this report

The growing popularity of eSports and competitive gaming has become a significant driver for the gaming accessories market. Tournaments such as IEM Cologne (CS: GO), ESL One (DOTA 2), League of Legends World Championship, and The International (DOTA 2) have gained significant recognition globally, gaining millions of fans. This growing popularity of e-sports tournaments is encouraging game developers and e-sports organizations to host their own events to enhance global reach and mainstream acceptance. These events also encourage gamers to upgrade their equipment to compete at higher levels or enhance their gaming experience as spectators.

Moreover, several countries are actively supporting the eSports market by organizing national tournaments and events. For instance, in July 2025, Saudi Arabia announced the Esports World Cup, set to take place in Riyadh. This tournament is expected to feature the largest prize pool in eSports history and will showcase teams competing across various game genres. The Esports World Cup is part of Saudi Arabia’s National Gaming and eSports Strategy, which aims to increase the sector's contribution to the country's GDP by over 50 billion SAR (approximately USD 13.3 billion) and create more than 39,000 jobs by 2032. Such large-scale initiatives increase the need for gaming peripherals like controllers, headsets, keyboards, and specialized gaming chairs, as participants and spectators alike invest in premium accessories for an immersive experience.

Furthermore, in January 2024, the French government announced plans for a National Esports Strategy, which includes initiatives such as eSports visas for players, support for grassroots eSports, and the development of a more structured eSports ecosystem. This strategy aims to not only foster a larger pool of professional players but also encourage casual gamers to invest in gaming accessories to emulate the professional setup. These factors, along with the increasing demand for high-performance gaming accessories, such as headsets for communication, ergonomic chairs for long gaming sessions, customizable controllers, and RGB-enabled keyboards, are expected to drive the growth of the gaming accessories market during the forecast period.

Some of the developments in this market are as follows:

The integration of virtual reality (VR) and augmented reality (AR) technologies into gaming has transformed the industry, creating highly immersive and interactive experiences. AR and VR enhance the gaming experience by blending the real world with virtual elements. VR gaming immerses players in entirely virtual environments, while AR gaming overlays digital elements onto the real world, offering players unique and engaging gameplay. This evolution is driving significant demand for advanced gaming accessories designed to optimize these experiences.

AR adds digital components, such as virtual images and characters, to real-world settings using a phone’s camera or video viewer. Unlike VR, AR keeps players grounded in the real world, offering a partially immersive experience. Popular AR games include Zombies, Run!, Ingress, and Pokémon Go.

On the other hand, VR creates a fully virtual world that completely replaces the real environment, immersing users in a digitally created space. VR gaming requires a headset and computer hardware to produce this immersive experience, allowing players to engage in thrilling storylines filled with challenges and puzzles. As VR and AR gaming continue to gain mainstream popularity, demand for specialized accessories such as VR headsets, motion controllers, gloves, and treadmills has surged. These accessories allow players to interact with virtual environments seamlessly and with greater precision. For AR gaming, accessories like augmented reality glasses and smartphones optimized for AR games are rising in demand.

These factors, along with a growing library of VR and AR gaming content, advancements in hardware technology, and declining prices for VR headsets, are expected to drive the market’s growth in the coming years.

Some of the developments in this market are as follows:

A gaming accessory is a piece of hardware designed to enhance the gaming experience or facilitate the use of a video game system. Wireless gaming accessories, driven by advancements in connectivity technologies such as Bluetooth and Wi-Fi, have become the preferred choice for gamers at all levels, from casual players to e-sports professionals. This growing preference is driving demand for products such as wireless gaming headsets with surround sound and noise cancellation, wireless keyboards and mice with RGB lighting and programmable keys, and wireless controllers featuring haptic feedback and adaptive triggers.

Wireless gaming accessories offer greater freedom of movement, which is essential for gamers who prioritize comfort and flexibility during extended gaming sessions. Moreover, the availability of wireless charging technologies and longer battery life has addressed previous concerns over usability, making these products even more appealing. Many wireless accessories also support cross-platform compatibility, allowing players to use the same devices across consoles, PCs, and mobile devices.

As a result, gamers are increasingly investing in high-quality wireless products that enhance their experience without the constraints of wired connections. Factors such as the elimination of tangled wires, improved portability, low-latency connections, customizable options, and the growth of mobile and console gaming—where wireless devices are preferred—are further supporting the market's expansion. Additionally, ongoing technological advancements that reduce latency in wireless devices continue to fuel market growth.

Some of the developments in this market are as follows:

Based on product, the global gaming accessories market is segmented into gaming chairs, controllers, headsets & audio equipment, keyboards & mice, and other products. In 2025, the keyboards & mice segment is estimated to account for the largest share of the global gaming accessories market. The large share of this segment can be attributed to factors such as the emergence of gaming peripherals optimized for e-sports, the increasing adoption of mechanical and customizable gaming keyboards, advancements in ergonomic mouse designs for improved gaming performance, and the surge in online multiplayer games that demand precise controls.

These peripherals play a crucial role in PC gaming. In gaming, keyboards and mice offer faster response times, better speed, and enhanced performance compared to traditional input devices. Gaming keyboards are typically mechanical, featuring key switches that require less pressure for quicker actions. They may also include additional programmable keys for macros. Gaming mice are designed for comfort and precision, often with customizable settings such as adjustable sensitivity measured in dots per inch (DPI). A higher DPI setting enables faster movements, while a lower DPI setting allows for smaller, more precise movements.

However, the headsets & audio equipment segment is expected to register the highest CAGR during the forecast period of 2025 to 2032. Headsets and audio equipment play a crucial role in enhancing the immersive gaming experience, particularly in multiplayer and competitive gaming. Factors driving the growth of this segment include the increasing demand for immersive audio experiences in AAA games, the rise of online multiplayer games that require clear communication, advancements in noise-canceling and spatial audio technologies, and the growing popularity of wireless gaming headsets with extended battery life.

In 2025, Asia-Pacific is estimated to account for the largest share of the global gaming accessories market. Asia-Pacific’s significant market share can be attributed to the high concentration of gamers in China, India, Japan, and South Korea, the rapid growth of the e-sports and mobile gaming industries, large-scale investments in gaming infrastructure and e-sports tournaments, the availability of affordable gaming accessories due to local manufacturing, and the expansion of high-speed internet and 5G networks in both rural and urban areas contribute to the region’s dominant position in the gaming accessories market.

Moreover, the market in Asia-Pacific is projected to register the highest CAGR during the forecast period. The region's rapid internet penetration, increasing affordability of smartphones, and significant investments in gaming infrastructure are driving this robust growth.

The report includes a competitive landscape based on an extensive assessment of the key growth strategies adopted by leading market players over the past three years (2021-2025). The key players profiled in the global gaming accessories market report are Alienware (Dell) (U.S.), Logitech (Switzerland), Razer (Singapore), Corsair Memory Inc. (U.S.), Turtle Beach (U.S.), HyperX (HP Inc.) (U.S.), SteelSeries (Denmark), Sony Corporation (Japan), Mad Catz (U.S.), Nvidia Corporation (U.S.), Cooler Master (Taiwan), Sennheiser (Germany), Anker Innovations (China), Redragon (China), SADES Technological Corporation (China), Plantronics (U.S.), and Nintendo (Japan).

|

Particulars |

Details |

|

Number of Pages |

210 |

|

Format |

|

|

Forecast Period |

2025–2032 |

|

Base Year |

2024 |

|

CAGR (Value) |

7.1% |

|

Market Size (Value) |

USD 15.1 Billion by 2032 |

|

Segments Covered |

By Product

By Device Type

By Technology

By Distribution Channel

|

|

Countries Covered |

Europe (Germany, U.K., Italy, France, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Thailand, Singapore, Rest of Asia-Pacific), North America (U.S., Canada), Latin America (Brazil, Argentina, Mexico, Rest of Latin America), and the Middle East & Africa (UAE, Saudi Arabia, South Africa, Rest of the Middle East & Africa) |

|

Key Companies |

Alienware (Dell) (U.S.), Logitech (Switzerland), Razer (Singapore), Corsair Memory Inc. (U.S.), Turtle Beach (U.S.), HyperX (HP Inc.) (U.S.), SteelSeries (Denmark), Sony Corporation (Japan), Mad Catz (U.S.), Nvidia Corporation (U.S.), Cooler Master (Taiwan), Sennheiser (Germany), Anker Innovations (China), Redragon (China), SADES Technological Corporation (China), Plantronics (U.S.), and Nintendo (Japan). |

The global gaming accessories market size was valued at $8.9 billion in 2024.

The market is projected to grow from $9.4 billion in 2025 to $15.1 billion by 2032.

The gaming accessories market analysis indicates substantial growth, with projections indicating that the market will reach $15.1 billion by 2032 at a compound annual growth rate (CAGR) of 7.1% from 2025 to 2032.

The key companies operating in this market include Alienware (Dell) (U.S.), Logitech (Switzerland), Razer (Singapore), Corsair Memory Inc. (U.S.), Turtle Beach (U.S.), HyperX (HP Inc.) (U.S.), SteelSeries (Denmark), Sony Corporation (Japan), Mad Catz (U.S.), Nvidia Corporation (U.S.), Cooler Master (Taiwan), Sennheiser (Germany), Anker Innovations (China), Redragon (China), SADES Technological Corporation (China), Plantronics (U.S.), and Nintendo (Japan).

The growing consumer preference for wireless gaming accessories is a prominent trend in this market.

By product, the keyboards & mice segment is forecasted to hold the largest market share during 2025-2032.

By device type: the smartphones segment is forecasted to hold the largest market share during 2025-2032.

By technology, the wireless segment is forecasted to hold the largest market share during 2025-2032.

By distribution channel, the online segment is forecasted to hold the largest market share during 2025-2032.

By geography, the Asia-Pacific region is forecasted to hold the largest market share during 2025-2032.

By region, Asia-Pacific holds the largest share of the gaming accessories market in 2025. The market in Asia-Pacific is also projected to register the highest growth rate during the forecast period. Factors driving this growth include the increasing popularity of mobile gaming, a rise in e-sports tournaments, and growing investments in gaming infrastructure. Key countries such as China, Japan, South Korea, and India dominate the gaming landscape in Asia-Pacific, with significant contributions from both casual and professional gamers.

Key factors driving the growth of this market include the rising popularity of e-sports & competitive gaming, the expanding global gaming community, and the increasing demand for immersive gaming experiences through VR and AR.

Published Date: Feb-2026

Published Date: Nov-2024

Published Date: Feb-2026

Published Date: Sep-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates