Resources

About Us

DTC Food Market by Type (Food {Bakery & Confectionery, Meat, Poultry, & Seafood, Dairy, Snacks}, Beverages {Carbonated Soft Drinks & Juices, RTD Tea & Coffee, Alcoholic Beverages}), by Distribution Channel (Online, Offline) - Global Forecast to 2031

Report ID: MRFB - 1041087 Pages: 204 Jan-2024 Formats*: PDF Category: Food and Beverages Delivery: 2 to 4 Hours Download Free Sample ReportThe growth of this market is driven by the rising adoption of convenience foods, growing online purchases of food products, and the increasing number of DTC food brands. However, the lack of brand awareness & limited product offerings of DTC food providers, and product quality concerns & delivery delays are factors restraining the growth of this market to some extent. The growing demand for premium & personalized food products is expected to generate market growth opportunities. However, high competition from other distribution channels is a major challenge for the players operating in this market. Furthermore, consumers’ increasing focus on health and wellness is a major trend in the DTC food market.

The report offers a competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, and key growth strategies adopted in the last 3–4 years. Some of the key players operating in the DTC food market are Anheuser–Busch InBev NV/SA (Belgium), AriZona Beverages USA, LLC (U.S.), JBS S.A. (Brazil), Mondelēz International, Inc. (U.S.), Nestlé S.A. (Switzerland), OLIPOP, Inc (U.S.), PepsiCo, Inc. (U.S.), The Coca-Cola Company (U.S.), The Kraft Heinz Company (U.S.), The Naked Market (U.S.), and Unilever PLC (U.K.).

During the last decade, the food and beverage industry has transformed significantly due to growth in online grocery shopping and direct-to-consumer sales. Nowadays, consumers seek convenience and personalization in their food options. Online food purchases are increasing globally, resulting from consumers’ increasing access to the internet and growing smartphone usage. According to the Food and Agriculture Organization (FAO), e-commerce has skyrocketed in the food industry since 2020 due to the COVID-19 pandemic. Moreover, consumers’ increasing preference for purchasing food products online is driving a digital revolution in the food industry. Thus, growing urbanization, rising disposable incomes, changing lifestyles, and the increasing number of working professionals are driving online sales of food & beverage products.

DTC brands use their own websites for online sales, allowing them to establish direct relationships with consumers without the involvement of intermediaries. Thus, they can communicate directly with consumers, gather feedback, and build brand loyalty. Moreover, this also allows DTC food manufacturers to innovate and keep pace with trending consumer interests. For instance, consumers are growing increasingly interested in plant-based foods due to concerns such as environmental sustainability, food allergies & intolerances, and animal welfare. As a result, many food start-ups and some established key players are investing in plant-based foods, selling their products directly from their websites, and taking feedback from consumers. Food manufacturers are focusing on innovating their products with new flavors and ingredients to cater to consumer preferences. Online distribution is enabling DTC food brands to expand their reach beyond local markets and serve customers nationally and internationally. This shift to online sales is helping DTC food manufacturers broaden their customer bases and increase business sustainability. Thus, increasing online purchases are supporting the growth of the DTC food market.

Based on type, the global DTC food market is segmented into food and beverages. In 2024, the food segment is expected to account for the larger share of the global DTC food market. The large market share of this segment is attributed to the growing demand for convenience foods, changes in lifestyle and food habits, increasing consumer inclination towards online shopping, growing demand for nutritional and fortifying food products, rising innovative food products, and rising spending on healthy and nutritious diets.

However, the beverages segment is expected to register a higher CAGR during the forecast period of 2024–2031. The growth of this segment is mainly attributed to the rising consumer demand for healthier and more premium beverage products, changing consumer preferences, increasing demand for low-calorie beverages, and growing popularity for plant-based and functional beverages among consumers.

Based on distribution channel, the DTC food market is segmented into online distribution channel and offline distribution channel. In 2024, the online distribution channel segment is expected to account for the larger share of the DTC food market. The large market share of this segment is attributed to the increasing preference for online shopping among consumers, the convenience offered by online platforms, the growing penetration of the internet, and the high popularity among food and beverage manufacturers of creating websites to display and sell their products directly to consumers. Moreover, the growing preference for personalization, contactless shopping, consumer convenience, easy price comparisons between brands, the advantage of greater discounts compared to offline stores, and a greater product selection experience are some of the factors further increasing the popularity of the online distribution of the food and beverage products.

Moreover, this segment is further projected to register a higher CAGR during the forecast period of 2024–2031, as the COVID-19 pandemic has further accelerated the shift towards online shopping as consumers prioritize safety and contactless transactions.

Based on geography, the global DTC food market is divided into five major regions: North America, Asia-Pacific, Europe, Latin America, and the Middle East & Africa. In 2024, North America is expected to account for the largest share of the global DTC food market. The large market share of this region is mainly attributed to the growing consumer awareness and preference for direct-to-consumer food products, increasing popularity of online food purchasing, presence of a large number of key food and beverage brands following direct-to-consumer business models, and rising consumer awareness about the online platforms of the brands.

Additionally, this region is further slated to register the highest CAGR during the forecast period of 2024–2031. The fast growth of this region is mainly attributed to the rising technological advancements in online food distribution and high consumer preference for convenience and personalized shopping experiences. Moreover, factors such as busy lifestyles, increasing disposable income, and a growing demand for healthy and sustainable food options are also expected to support the high growth of the DTC food market in North America.

|

Particulars |

Details |

|

Number of Pages |

204 |

|

Format |

|

|

Forecast Period |

2024–2031 |

|

Base Year |

2023 |

|

CAGR |

18.7% |

|

Estimated Market Size (Value) |

$195.39 Billion by 2031 |

|

Segments Covered |

By Type

By Distribution Channel

|

|

Countries Covered |

North America (U.S., Canada), Europe (U.K., Germany, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and the Middle East & Africa |

|

Key Companies |

Anheuser–Busch InBev NV/SA (Belgium), AriZona Beverages USA, LLC (U.S.), JBS S.A. (Brazil), Mondelēz International, Inc. (U.S.), Nestlé S.A. (Switzerland), OLIPOP, Inc (U.S.), PepsiCo, Inc. (U.S.), The Coca-Cola Company (U.S.), The Kraft Heinz Company (U.S.), The Naked Market (U.S.), and Unilever PLC (U.K.) |

DTC or Direct-to-Consumer refers to a business model where a food company sells its products directly to consumers without relying on any third-party retailers, wholesalers, or other intermediaries (E-commerce websites). In the context of the food market, DTC food refers to food products that are sold directly to consumers by the manufacturers/producers themselves, typically through online platforms and physical stores owned by the food producers. This market encompasses various food and beverage products, including snacks, bakery products, dairy, fresh produce, meat, specialty items, and beverages, all of which are offered directly to consumers through their own websites and physical stores.

In this Global DTC Food Market study, the market size in terms of value is calculated by considering the revenue generated by food and beverage product manufacturers by selling their food and beverage products directly to consumers only through their website and at their exclusive stores at the global level. This study primarily provides a detailed market assessment and valuable insights (in terms of value) for the DTC food and beverage products, including type, distribution channel, and various countries across the different regions.

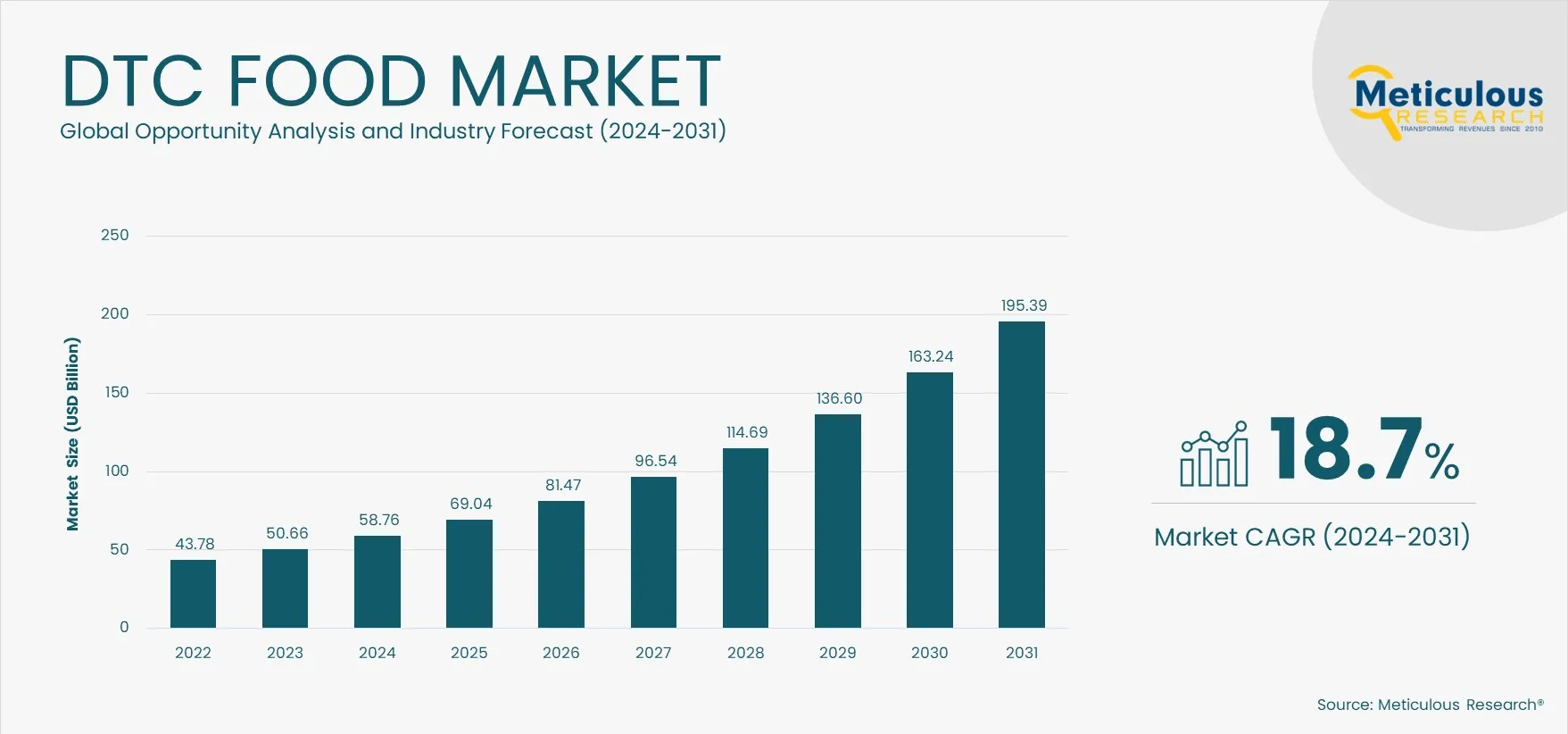

The DTC food market is projected to reach $195.39 billion by 2031, at a CAGR of 18.7% during the forecast period 2024–2031.

Based on distribution channel, the online distribution channel segment is projected to record a higher growth rate during the forecast period 2024–2031.

o Rising Adoption of Convenience Foods

o Growing Online Purchases of Food Products

o Increasing Number of DTC Food Brands

o Lack of Brand Awareness & Limited Product Offerings of DTC Food Providers

o Product Quality Concerns & Delivery Delays

The key players operating in the DTC food market are Anheuser–Busch InBev NV/SA (Belgium), AriZona Beverages USA, LLC (U.S.), JBS S.A. (Brazil), Mondel?z International, Inc. (U.S.), Nestlé S.A. (Switzerland), OLIPOP, Inc (U.S.), PepsiCo, Inc. (U.S.), The Coca-Cola Company (U.S.), The Kraft Heinz Company (U.S.), The Naked Market (U.S.), and Unilever PLC (U.K.).

North America is projected to record the highest CAGR during the forecast period due to the rising technological advancements in online food distribution and high consumer preference for convenience and personalized shopping experiences. Moreover, factors such as busy lifestyles, increasing disposable income, and a growing demand for healthy and sustainable food options are also expected to support the high growth of the DTC food market in North America.

Published Date: Oct-2024

Published Date: Sep-2024

Published Date: Jun-2024

Published Date: Mar-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates