Resources

About Us

AI-Driven Battery Management Systems Market by Component (Hardware, Software, Services), Application (Electric Vehicles, Energy Storage), Distribution Channel, End User, and Geography - Global Forecast to 2032

Report ID: MRSE - 1041474 Pages: 285 Apr-2025 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportReport Overview

This comprehensive market research report analyzes the rapidly expanding AI-driven battery management systems market, evaluating how artificial intelligence and machine learning technologies are transforming traditional battery management to optimize performance, extend lifecycles, and enhance safety across various applications. The report provides a strategic analysis of market dynamics, growth projections till 2032, and competitive positioning across global and regional/country-level markets.

Market Dynamics Overview

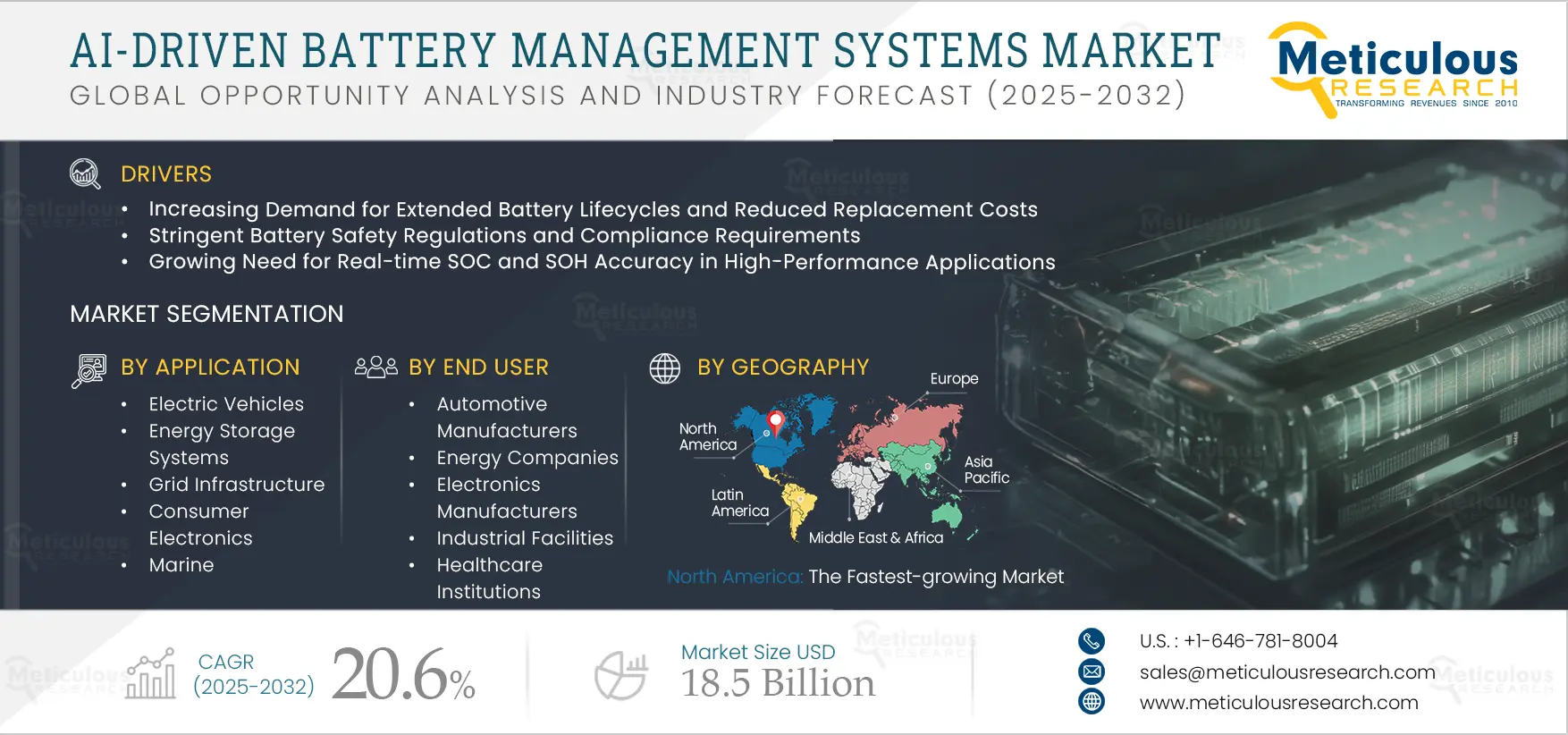

Key Market Drivers & Trends

The AI-driven battery management systems (BMS) market is primarily driven by increasing demand for longer battery lifecycles, stringent safety regulations, the need for precise state-of-charge (SOC) and state-of-health (SOH) estimations, and the growing adoption of fast charging technologies that require advanced thermal management solutions. The shift from hardware-centric to software-defined BMS solutions is reshaping the industry, while the integration of digital twin technology for predictive battery modeling is gaining significant attention. Additionally, the adoption of wireless BMS architectures for weight reduction and the rise of performance-based licensing models are further accelerating the market growth, especially in electric vehicle (EV) and renewable energy applications.

Key Challenges

Despite growth prospects, the overall AI-driven battery management systems market faces challenges including high initial investment required for R&D and algorithm development, difficulties in collecting and standardizing battery data, and the ongoing challenge of balancing edge computing with cloud-based processing. Additionally, retrofitting AI capabilities into existing battery systems presents technical complexities, and verifying the performance and reliability of AI algorithms remains a significant barrier, potentially slowing down market penetration.

Click here to: Get a Free Sample Copy of this report

Click here to: Get a Free Sample Copy of this report

Growth Opportunities

The AI driven battery management systems market offers several high-growth opportunities. The rise of second-life battery applications, driven by circular economic initiatives that are opening new avenues for repurposed battery usage. Another major opportunity lies in vehicle-to-grid (V2G) integration, which demands advanced BMS intelligence and holds strong potential for utility-scale deployments. Additionally, the growing adoption of Battery-as-a-Service (BaaS) models is helping reduce upfront capital expenditure while ensuring efficient, long-term battery performance. The development of multi-chemistry BMS solutions to support a wide range of applications, along with tailored offerings for emerging markets, further expands the growth landscape for both manufacturers and software developers.

Market Segmentation Highlights

By Component

The software and AI solutions segment is expected to dominate the overall AI-driven battery management systems market in 2025, primarily due to the growing adoption of predictive analytics and state estimation algorithms. These software components are essential for optimizing battery performance and ensuring safety, with key modules including state-of-charge (SOC), state-of-health (SOH), and remaining useful life (RUL) estimations, along with thermal management systems and cell balancing algorithms. These tools enhance decision-making, enable predictive maintenance, and support the overall efficiency of battery systems, especially critical in EV and energy storage applications. However, the Hardware segment is expected to witness a faster growth rate through 2032, driven by increasing demand for real-time, on-device processing. AI-optimized BMS processors are becoming vital for enabling edge computing, which minimizes latency and enhances system responsiveness. This shift is especially important for applications that require immediate data handling, such as electric vehicles and grid-scale storage. Additionally, the integration of advanced sensors and monitoring systems, used for precise data collection and real-time battery diagnostics is further fueling hardware demand.

Based on services, the implementation & integration services segment is expected to hold the largest share of the overall AI driven battery management systems market in 2025, due to the challenges involved in seamlessly incorporating AI technologies into existing battery infrastructures. These services are critical for ensuring compatibility, system reliability, and optimal performance during deployment. AI Model Training & Customization also represents significant market growth, driven by the growing need to tailor algorithms for specific applications, chemistry, and usage conditions. However, Data Analytics Services are expected to experience the highest growth rate through 2032, primarily driven by the increasing importance of leveraging battery performance data to gain actionable insights, enhance operational decision-making, and support predictive maintenance strategies. As organizations seek to transform raw battery data into strategic intelligence, demand for advanced analytics capabilities is set to surge the market growth.

By Application

The electric vehicles segment is expected to hold the largest share of the AI-driven battery management systems market in 2025, primarily driven by the need for better range, fast charging, and enhanced battery safety in the automotive sector. Energy Storage Systems are also growing significantly, especially in large-scale utility projects due to their role in stabilizing the grid, supporting renewable energy, managing peak demand, and improving energy resilience. However, the Data Centers segment is expected to grow at fastest rate during the forecast period, due to the critical need for uninterrupted power and precise battery monitoring in backup systems as AI enhanced BMS ensures real time battery health insights, predictive maintenance, and optimized energy usage, reducing downtime risks and operating costs.

By Distribution Channel

The direct channel leads the market now because AI-driven BMS solutions, primarily driven by the need for high customization and deep technical integration, especially in complex applications like electric vehicles, aerospace, and utility-scale storage. However, the indirect channel is experiencing the fastest growth during the forecast period due to the increasing standardization and maturity of AI driven battery management systems technologies. As solutions become more modular and easier to integrate, system integrators and solution providers are playing a larger role in delivering battery management systems to markets like commercial energy storage and industrial systems.

By End User

The automotive manufacturers segment is expected to hold the largest share of the global AI driven battery management systems market in 2025, primarily due to their early and largescale adoption of advanced battery technologies to support electric mobility. Energy Companies follow closely, leveraging AI battery management systems to enhance grid storage and renewable energy integration. On other hand, the data centers segment is expected to experience the fastest growth rate during the forecast period, driven by rising power density demands, escalating energy costs, and the vital need for uninterrupted power to support digital infrastructure. Meanwhile, Industrial Facilities and the telecommunications sector are also emerging as strong growth areas, as intelligent battery systems become increasingly important for maintaining operational continuity and managing long term energy expenses.

By Geography

North America is expected to hold the largest share of the global AI driven battery management systems market in 2025, followed by Europe, due to rising adoption of electric vehicles, significant R&D investments, and strong regulatory frameworks supporting battery safety and efficiency. However, the Asia Pacific region especially China, South Korea, and Japan is witnessing the fastest growth rate during the forecast period, primarily driven by large scale EV production, proactive government initiatives to advance battery technologies, and rising deployments of energy storage systems. Meanwhile, the Middle East & Africa region is showing significant growth potential, particularly due to many industries in this region focusing on modernizing grid infrastructure and integrating renewable energy sources.

Competitive Landscape

The global AI-driven battery management systems market features a diverse competitive landscape with established battery manufacturers and semiconductor companies expanding AI capabilities alongside innovative software-focused startups gaining significant market share.

Established Consumer Goods Companies

CATL (Contemporary Amperex Technology Co., Limited) leads the market among established players, offering a broad range of AI-enabled battery management solutions that support various battery chemistries and applications. LG Energy Solution, Ltd. has strengthened its market position by integrating proprietary algorithms that enhance cell-level optimization and enable predictive maintenance. Panasonic Holdings Corporation maintains a strong market presence through its long-standing collaborations with automotive OEMs and energy storage providers. These companies primarily compete based on large-scale manufacturing capabilities, robust hardware-software integration, and well-established customer relationships across diverse sectors

Independent Sustainable Manufacturers

Tesla, Inc. has significantly disrupted the AI-driven BMS market with its vertically integrated model, combining proprietary hardware and self-learning algorithms refined through extensive real-world data. TWAICE Technologies GmbH has gained strong industry recognition for its battery analytics software, offering cloud-based predictive maintenance and lifecycle insights. Siemens AG stands out through its advanced use of digital twin technology, particularly in industrial and grid-scale battery applications. These tech-driven players primarily compete on the precision of their algorithms, adaptive learning capabilities, and the flexibility of their software to integrate with diverse battery systems.

The broader manufacturing landscape is evolving through growing collaboration between battery producers and AI software developers, while semiconductor companies are increasingly investing in specialized processors tailored for battery management tasks. Leading manufacturers are shifting toward cloud-to-edge architectures, enabling real time local processing while continuously improving AI algorithms through fleet wide learning.

As the market matures, manufacturers will need to address data ownership and privacy concerns, establishing standardized performance metrics for evaluating AI algorithms, and delivering cost-effective solutions that demonstrate clear ROI beyond early adopters. To achieve extensive adoption, successful companies must strike a balance between offering advanced AI capabilities and ensuring seamless, practical implementation across a wide range of battery applications.

|

Particulars |

Details |

|

Number of Pages |

285 |

|

Format |

PDF & Excel |

|

Forecast Period |

2025–2032 |

|

Base Year |

2024 |

|

CAGR (Value) |

20.6% |

|

Market Size (Value)in 2025 |

USD 4.1 Billion |

|

Market Size (Value) in 2032 |

USD 18.5 Billion |

|

Segments Covered |

By Component

By Application,

By Distribution Channel,

By End User,

|

|

Countries Covered |

North America (U.S., Canada) |

|

Key Companies |

CATL (Contemporary Amperex Technology Co., Limited), LG Energy Solution, Ltd., Panasonic Holdings Corporation, Tesla, Inc., Samsung SDI Co., Ltd., BYD Company Limited, Siemens AG, Texas Instruments Incorporated, Analog Devices, Inc., NXP Semiconductors N.V., Northvolt AB, Infineon Technologies AG, TWAICE Technologies GmbH, ABB Ltd., and Bosch Mobility Solutions (Robert Bosch GmbH). |

The global AI-driven battery management systems market was valued at $3.4 billion in 2024. This market is expected to reach $18.5 billion by 2032 from an estimated $4.1 billion in 2025, at a CAGR of 20.6% during the forecast period of 2025–2032.

The global AI-driven battery management systems market is expected to grow at a CAGR of 20.6% during the forecast period of 2025–2032.

The global AI-driven battery management systems market is expected to reach $18.5 billion by 2032 from an estimated $4.1 billion in 2025, at a CAGR of 20.6% during the forecast period of 2025–2032.

The key companies operating in this market include CATL (Contemporary Amperex Technology Co., Limited), LG Energy Solution, Ltd., Panasonic Holdings Corporation, Tesla, Inc., Samsung SDI Co., Ltd., BYD Company Limited, Siemens AG, Texas Instruments Incorporated, Analog Devices, Inc., NXP Semiconductors N.V., Northvolt AB, Infineon Technologies AG, TWAICE Technologies GmbH, ABB Ltd., and Bosch Mobility Solutions (Robert Bosch GmbH).

Major trends shaping the market include shift from hardware-centric to software-defined BMS solutions, integration of digital twin technology for predictive battery modeling, wireless BMS architecture adoption, edge AI processors optimized for battery applications, and performance-based BMS licensing models.

North America leads the global market, followed by Europe, due to advanced electric vehicle adoption, substantial R&D investments, and strong regulatory push for battery performance. Asia-Pacific is witnessing the highest growth rate driven by massive manufacturing scale and government initiatives.

The growth of this market is driven by increasing demand for extended battery lifecycles, stringent safety regulations, growing need for SOC and SOH accuracy, rising adoption of fast charging technologies requiring advanced thermal management, and pressure to reduce battery warranty claims and recalls.

Published Date: Jun-2023

Published Date: Jun-2023

Published Date: Oct-2022

Published Date: Sep-2024

Published Date: Aug-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates