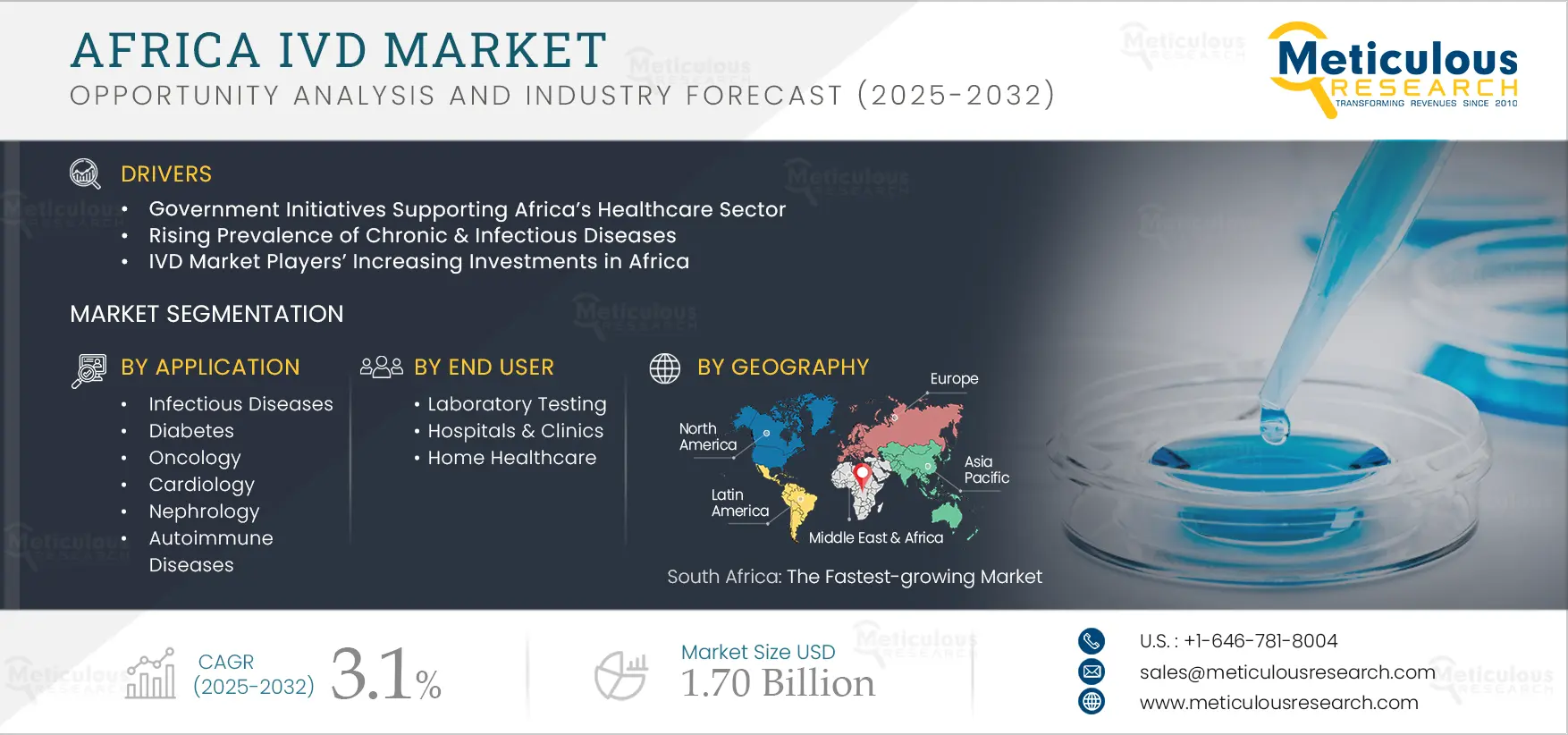

The Africa IVD Market is expected to grow at a CAGR of 3.1% from 2024 to 2031 to reach $1.65 billion by 2031. The Africa IVD Market includes kits & reagents, instruments, and software & services. The growth of the Africa IVD market is driven by factors such as the rising prevalence of chronic & infectious diseases, IVD market players’ increasing investments in Africa, the growing demand for Point-of-care (POC) & rapid diagnostics, the rising geriatric population, government initiatives supporting Africa’s healthcare sector, rising healthcare expenditure, and increasing R&D expenditure.

Moreover, increasing awareness regarding the importance of early diagnosis, advances in genomics & proteomics, and the increasing adoption of personalized medicine are expected to generate growth opportunities for the players operating in the Africa IVD market.

Here are the top 10 companies operating in the Africa IVD Market

F. Hoffmann-La Roche Ltd (Switzerland)

Founded in 1896 and headquartered in Basel, Switzerland, F. Hoffmann-La Roche Ltd is a research-based healthcare company that provides diagnostics solutions. The company operates through two major business segments: Pharmaceuticals and Diagnostics. Through the Diagnostics segment, it offers centralized and point-of-care reagents and kits, advanced staining reagents, molecular diagnostic tests, and blood screening tests.

The Diagnostics segment is further categorized into Core Lab, Molecular Lab, Point of Care, Diabetes Care, and Pathology Lab. This segment manufactures equipment & reagents for research & medical diagnostic applications.

F. Hoffman-La Roche has 20 manufacturing sites and 27 research & development sites engaged in Pharmaceuticals and Diagnostics operations worldwide.

Some of its subsidiaries operating in the Africa IVD market market are F. Hoffmann-La Roche AG (Russia), Roche Algerie SPA (Algeria), Hoffmann-La Roche Ltd (Côte d’Ivoire), and Roche Kenya Limited (Kenya).

Abbott Laboratories (U.S.)

Founded in 1888 and headquartered in Illinois, the U.S., Abbott Laboratories develops, manufactures, and markets healthcare products. The company offers a wide range of products in diagnostics, medical devices, nutrition, and branded generic pharmaceuticals markets. Abbott operates worldwide through four business segments: Established Pharmaceutical Products, Diagnostic Products, Nutritional Products, and Medical Devices.

The company operates in the Africa IVD market through its Diagnostic Products business segment, which is further divided into Core Laboratory, Rapid Diagnostics, Point of Care, and Molecular business segments. The Rapid Diagnostics business is part of Alere Inc. (U.S.), a diagnostic device manufacturer and service provider that Abbott acquired in October 2017. Abbott Laboratories has a geographical presence and a strong distribution network through direct and indirect channels in several countries, including in Africa.

The company has 90 manufacturing facilities globally, of which 24 manufacturing sites are engaged in developing diagnostic products. Some of its subsidiaries operating in Africa include Abbott Kenya Limited (Kenya), Abbott Laboratories South Africa (Pty) Ltd. (South Africa), and Alere Healthcare Nigeria Limited (Nigeria).

Danaher Corporation (U.S.)

Established in 1984 and headquartered in Washington, D.C., the U.S., Danaher Corporation designs, manufactures, and markets medical, professional, industrial, and commercial products & services. The company operates in three segments: Life Sciences, Diagnostics, and Biotechnology.

Danaher operates in the Africa IVD market through the Diagnostics business segment. The Diagnostics segment offers a wide range of in-vitro diagnostics products, including analytical instruments, reagents, consumables, software, and services. These products are used in various healthcare settings such as hospitals, physicians’ offices, reference laboratories, and other critical care settings to diagnose diseases. This segment is further categorized into Clinical Lab Diagnostics, Critical Care Diagnostics, and Anatomical & Pathological Diagnostics.

Danaher Corporation has 212 R&D, manufacturing, sales, distribution, service, and administrative facilities in more than 60 countries worldwide. The company’s manufacturing facilities are located in North America, Europe, Asia, and Australia. Danaher Corporation has several subsidiaries worldwide, of which Beckman Coulter, Inc. (U.S.), Cepheid (U.S.), Leica Biosystems Nussloch GmbH (Germany), HemoCue AB (Sweden), and Radiometer Medical ApS (Denmark) offer instruments & reagents for in-vitro diagnostic applications.

Becton, Dickinson and Company (U.S.)

Founded in 1887 and headquartered in New Jersey, the U.S., Becton, Dickinson and Company (BD) manufactures and sells a wide range of medical devices, laboratory equipment, and diagnostic products used by healthcare institutions, clinical laboratories, pharmaceutical companies, and research centers. The company operates in three business segments: BD Medical, BD Life Sciences, and BD Interventional.

The BD Life Sciences business segment offers products through two major categories, namely, Integrated Diagnostic Solutions (Diagnostic Systems and Preanalytical Systems) and Biosciences. The Diagnostic Systems category offers numerous products with clinical and industrial applications. These products include molecular testing systems for infectious diseases & women’s health, liquid-based cytology systems for cervical cancer screening, culturing systems, rapid diagnostic assays for testing respiratory infections, microorganism identification, and drug susceptibility systems.

BD has a direct presence in the U.S., Brazil, Canada, China, France, Spain, the U.K., Germany, Hungary, India, Ireland, Israel, Italy, Japan, Mexico, Singapore, the Netherlands, South Africa, Egypt, Zambia, Kenya, and Ghana, among others through its manufacturing, sales operations, offices, and subsidiaries. The R&D facilities of the company are located in China, France, India, Ireland, the U.S., and Singapore. BD has a wide global distribution network and markets its products through independent distribution channels and directly to hospitals, healthcare institutions, and independent sales representatives. Some of the subsidiaries operating in Africa include BD (West Africa) Limited (Ghana), Becton Dickinson East Africa Ltd. (Kenya), and Becton Dickinson (Pty) Ltd. (South Africa).

bioMérieux SA (France)

Founded in 1963 and headquartered in Marcy-l’Étoile, France, bioMérieux develops a wide range of products & solutions, including reagents, instruments, and software for clinical diagnostics. The company offers products for microbiology, immunoassay, molecular biology, and industrial applications. The company operates through two business segments Clinical Applications and Industrial Applications business segments. The company operates in the Africa IVD market through its Clinical Applications business segment. The Clinical Applications segment is further categorized into Molecular Biology, Microbiology, Immunoassays, and Other Ranges. The products offered by this segment are used to diagnose infectious diseases such as bacterial infections, parasitic infections, and viral infections.

The company has a geographical presence and a distribution network across 160 countries through its 44 subsidiaries and 15 production sites. The activities carried out at these sites are the production, sales, and distribution of reagents for ready-to-use media for microbiology and industrial applications, research & development, and commercial and administrative functions. The major subsidiaries of company operating in Africa are bioMérieux South Africa Pty Ltd. (South Africa), bioMérieux Algérie E.u.r.l. (Algeria), bioMérieux Kenya Ltd. (Kenya), and bioMérieux West Africa SAU (Côte d’ivoire).

Siemens Healthineers AG (Germany)

Founded in 1847 and headquartered in Erlangen, Germany, Siemens Healthineers AG develops and sells a wide range of products, including medical imaging applications, laboratory diagnostics, and point-of-care testing. The company also offers digital health platforms for various clinical specialties and laboratories worldwide.

Siemens Healthineers operates in four business segments: Imaging, Diagnostics, Varian, and Advanced Therapies. The company operates in the in vitro diagnostics market through its Diagnostics segment, which offers in vitro diagnostic products and services to healthcare professionals in molecular diagnostics, point-of-care diagnostics, and laboratories.

Siemens has a direct presence in more than 70 countries, including the U.S., Canada, Germany, the U.K., France, Italy, Spain, Denmark, Sweden, Switzerland, Belgium, India, China, Japan, Australia, New Zealand, and the Republic of Korea. Some of the major subsidiaries operating in the Africa IVD market are Siemens Healthcare (South Africa), Varian Medical Systems Africa (Pty) Ltd. (South Africa), Siemens Healthcare Proprietary Limited (South Africa), Varian Medical Systems Algeria Spa., (Algeria), and VMS Kenya, Ltd, (Kenya).

QIAGEN N.V. (Netherlands)

Founded in 1984 and headquartered in Venlo, Netherlands, QIAGEN develops and sells instruments, consumables, and digital bioinformatics solutions for oncology, infectious diseases, sexual and reproductive health, TB management, precision diagnostics, and point-of-care testing research. The company operates in two business segments: Molecular Diagnostics and Life Sciences. The Molecular Diagnostics segment offers a wide range of molecular diagnostic technologies, including automated systems, assays, markers, and reagents used to diagnose cancer and infectious diseases.

QIAGEN offers its products to more than 500,000 customers and has 35 subsidiaries operating across 25 countries, including the U.S., Canada, Germany, Spain, the U.K., France, Italy, the Netherlands, Sweden, Turkey, Sweden, Brazil, Mexico, China, Hong Kong, Taiwan, South Korea, India, and South Africa. Qiagen has manufacturing and production facilities in the U.S., Germany, China, and the U.K.

The company has a distribution network through its partners across 60 countries worldwide and operates in the African IVD market through its subsidiary, QIAGEN SA (Pty)–Ltd South Africa.

Thermo Fisher Scientific Inc. (U.S.)

Founded in 1956 and headquartered in Massachusetts, the U.S., Thermo Fisher Scientific Inc. is a biotechnology company engaged in life sciences research. The company operates through four business segments: Life Sciences Solutions, Analytical Instruments, Specialty Diagnostics, and Laboratory Products and Biopharma Services. The company operates in the Africa IVD market through its Specialty Diagnostics segment. It offers diagnostic test kits, reagents, culture media, instruments, and associated products for customers in healthcare, clinical, pharmaceutical, industrial, and food safety laboratories.

Some of Thermo Fisher’s major brands are Thermo Scientific, Applied Biosystems, Invitrogen, Fisher Scientific, Unity Lab Services, and Patheon. In June 2019, Thermo Fisher Scientific sold its Anatomical Pathology business to PHC Holdings Corporation (Japan), which primarily offered products for cancer diagnosis and medical research in histology, cytology, and hematology applications.

The company has a direct presence through its regional offices and production sites in the U.S., Mexico, Brazil, Germany, Belgium, Austria, the U.K., Italy, the Netherlands, South Africa, the UAE, India, China, Japan, Australia, and the Republic of Korea. Some of the major subsidiaries of the company are Thermo Electron (Proprietary) Limited (South Africa), Thermo Electron Corporation (Proprietary) Limited (South Africa), and Winter Breeze Trading 129 Pty. Ltd (South Africa).

Bio-Rad Laboratories, Inc. (U.S.)

Founded in 1952 and headquartered in California, the U.S., Bio-Rad Laboratories, Inc. distributes and manufactures clinical diagnostics products and is engaged in life sciences research. The company supplies and produces various systems and products for healthcare, analytical chemistry, and life sciences research. Bio-Rad Laboratories operates through two reportable segments: Clinical Diagnostics and Life Sciences. Bio-Rad operates in the Africa IVD market through its Clinical Diagnostic Segment. The company provides over 3,000 products through the Clinical Diagnostic segment, comprising over 300 clinical diagnostics tests, including IVD. The company’s offerings cater to physician offices, diagnostic reference laboratories, hospital laboratories, and transfusion laboratories.

The company has a direct distribution channel in more than 35 countries outside the U.S., including Algeria, Ghana, Malawi, Tanzania, Nigeria, South Africa, and Uganda, through its subsidiary, Bio-Rad Laboratories (Pty) Limited (South Africa).

Illumina, Inc. (U.S.)

Founded in 1998 and headquartered in California, the U.S., Illumina, Inc. develops and markets sequencing and array-based solutions for genomic analysis. The company operates its business in two segments: Core Illumina and Grail. Through its Core Illumina segment, the company operates in the Africa IVD market by providing NGS platforms for diagnostic use. It offers solutions and services to molecular diagnostic laboratories, government laboratories, academic institutions, hospitals, genomic research centers, biotechnology companies, consumer genomics companies, pharmaceuticals, and commercial companies.

The Core Illumina segment includes all of Illumina’s core operations. The company markets and distributes products directly to customers in North America, Latin America, Europe, and Asia-Pacific. Additionally, it has a network of life-science distributors in certain markets within Europe, Asia-Pacific, Latin America, the Middle East, and Africa. In April 2020, the company donated sequencing systems and related consumables worth USD 1.4 million to support COVID-19 surveillance across 10 African countries, including the Democratic Republic of Congo, Ethiopia, Egypt, Ghana, Mali, Kenya, Nigeria, South Africa, Senegal, and Uganda.